This is part of a series on building your career in venture capital:

- Reading list for working in private equity/venture capital, including all of the major online communities, programs, and educational options for people studying VC

- How to win consulting, board, operating, and investment roles with private equity and venture capital funds (video)

- How to find a job as a VC scout

- How to get a job in venture capital

- VC recruiters list and compensation data

- How to negotiate a partner role at a VC or private equity firm

- For emerging VC and private equity investors: accelerators, platforms, communities, and incubators

- Syllabus for how to launch, manage, and invest a VC fund

Would you like to work with private equity and venture capital funds?

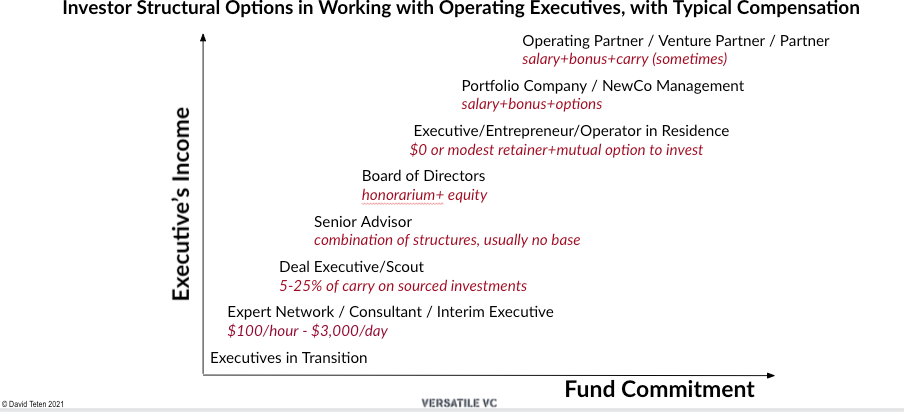

There are relatively few jobs directly inside private equity and venture capital funds, and those jobs are highly competitive. (See How to negotiate a partner role at a VC or private equity firm.) However, there are many other ways you can work with and earn money from the industry. You can work as a consultant, an interim executive, a board member, a deal executive partnering to buy a company, an executive in residence, or as an entrepreneur in residence. Not surprisingly, the tighter your relationship with the firm, typically the more money you will earn:

Here’s a video of a presentation and discussion on this topic which I led for GoingVC; the full deck is embedded at the bottom of this page.

In my past life, I’ve used all these models to work with talented business and technical leaders. I also manage Founders’ Next Move, a selective, free community for tech founders researching their next move.

Venture capitalists often come from an operating background. However, historically most private equity professionals were former investment bankers and other finance professionals. Then private equity players gradually realized that value cannot be created through financial engineering alone. A BCG study of 121 investments found that operational improvement drives 48% of value creation in PE-backed companies. PE funds now almost always require an upgrade in management and change management teams if necessary.

The simplest path forward is to identify funds in your industry of expertise, and reach out. You can explore all of the models below with them. First, start by identifying the firms which are investors in companies with which you have work history. Second, more broadly, look for investors in the industries in which you have expertise. You can identify institutional investors through one of multiple online databases:

| All Investors | Private Equity | Venture Capital |

Expert Networks

Expert Network firms source subject matter experts from various domains and pair them with clients seeking topical or industry insights. They typically charge clients $600-$2,000 per hour, and pay the expert $100 to $500 an hour. (I founded Circle of Experts, an expert network which I sold to Evalueserve.)

The expert network industry has grown an average 4.5% annually between 2015 and 2020, its market size topping $1.3B in 2020. While the major clients were initially hedge funds and private equity firms, consulting firms now comprise 32% of total demand for expert network services.

Inex One, an Expert Network marketplace, has compiled a list of 80 Expert Networks, summarized in the graphic below:

The largest expert networks are:

- GLG, accounting for approximately 50% of the industry’s revenue.

- AlphaSights, the second biggest generalist Expert Network after GLG.

- Guidepoint services 6 major categories of clients globally, across several industries.

- Third Bridge hires and retains talent to “democratise the world’s human insights and upend the traditional research model.”

Other notable expert networks include Atheneum Partners, Coleman Research Group, Dialectica, ENG, Lynk Global, Mosaic, PreScouter, ProSapient, and Tegus. There are also expert networks with sector or geography specialization. For example:

- SERMO is a social media network for physicians globally to exchange knowledge and share challenging patient cases.

- Clarity.fm connects startups to experts in building new businesses.

- The Expert Institute helps law firms and lawyers find expert witnesses for legal cases.

- Kingfish Group specializes in servicing the private equity industry.

- CAPVision is a primary research firm with a strong focus on Asia.

As an independent consultant, working with expert networks allows you to interact and learn from professional investors, industry consultants, and corporations; earn competitive compensation; and receive referral fees for introducing colleagues. Typically you’ll share your expertise in 5 main ways: phone calls, presentations/in-person meetings, surveys, white papers, and in-depth consulting projects.

Joining an expert network also saves you both time and financial resources. There is no membership fee to obtain access to potential projects with the expert network’s clients. There are also minimal marketing costs. While you should be proactive about being top-of-mind for the kind of projects you’d like to work on, the expert network will pair you with a client, if there’s a match. You also don’t have to spend time on negotiating or chasing payment, as the client pays upfront and the firm takes care of this for you.

These kinds of engagements also offer plenty of flexibility. The networks’ expectations towards you are minimal: once the expert network finds a fit between your expertise and a client’s knowledge requirements, they will send a request which you can accept or reject within 48 hours (usually). For confidentiality reasons, the consultation is held strictly between the client and the subject matter experts. Given that you are hired on a per-hour or per-project basis, there is no fixed obligation of time.

The criteria for offering your consulting services through an expert network are fairly specific, and summarized below:

| Attributes the Network Seeks | How the Network Assesses You |

| Relevant experience |

|

| Access to unique knowledge |

|

| Communication skills |

|

The expert networks usually don’t value social and management skills, as experts are mainly hired for the knowledge they possess, not for political or sales skills. This is good news for some people.

The key to success when working with expert and consultant networks? For starters, a detailed, up-to-date profile. Ensure that you’re putting your best, digital foot forward on Linkedin and your personal website by:

- Currency. Keep your availability and biography up-to-date.

- Quantify your achievements. When writing your bio, the standard format is: “Achieved X by doing Y, which resulted in Z (a number, $, etc.).” For more, see how to write a biography that sells.

- Explain how you acquired your expertise, which helps in increasing people’s perception of your legitimacy.

- Keywords. Make sure to mention firms you have touched in the past – past employers, clients, or service providers. Also it’s a good idea to use the terms that are specific to your industry, for example, industry jargon or technical terms.

There are a few additional steps you can take to win more consultations:

- Apply for open projects, which are listed on the system and also typically pushed to you via email.

- Mail your liaison when you have insight into a hot topic – for example, breaking news or a conference you just attended.

- Go on-call, i.e., indicate you’re available on short notice for any immediate needs clients have.

To set your rate, the Networks will typically suggest a modest figure, e.g., $200/hour. You’re not beholden to this. If you have unique expertise, the Network REALLY needs you and is not very price sensitive. If hundreds of people have your expertise, then your rate needs to drop to something in the range of their suggested figure. My record: I once paid someone £5,000 an hour. The client wanted his expertise; he was one of the top 5 people in the world in his domain (pharmaceutical M&A); so I had to pay it. Another example: a lobbyist for U.S. multinational companies in China writes about how his knowledge of U.S.-China relations and Chinese commercial policy experience allows him to charge between $400 and $1000 hourly for a call.

When you’re in a consultation, we recommend follow these guidelines:

- Ask questions to understand the client’s hot buttons & make sure to answer them.

- Observe compliance restrictions tightly.

- Review current news. As a subject matter expert, you’re expected to stay on top of recent developments in your field of knowledge.

- Acknowledge your limits. It is better to be upfront about what you don’t know or can’t do, than to improvise and risk disappointing the client.

- Offer referrals (via the expert network). The client is then able to obtain specifically what they need, and typically you’ll earn a referral fee.

As a next step, we recommend that you register at the major expert network websites, as well as LinkedIn and job boards, if you haven’t already. Make sure to include your biography and resume. You could also consider becoming a public expert: Profnet and HelpAReporter connect subject matter experts to journalists needing an expert opinion for an article or news piece.

To learn more about this space, see Civic’s report on The Rise of the Expert Economy.

Interim Executives and Consultant Networks

Interim executives typically engage in projects of 2-6 months duration, as opposed to engaging in short phone calls like experts from expert networks. A few, well-known networks include Business Talent Group, Catalant, Eden McCallum (focus on UK and the Netherlands), EIM, Eleven Canterbury, Expert360 (Australia), ForteOne, HighPoint Associates, Impact Executives (UK), SMA, Talmix (UK), Umbrex, and 10EQS.

Particularly relevant is Startups.com, which help tech startups identify consultants with relevant domain expertise. Bolster is an “on-demand executive talent marketplace” focused on “startups and scaleups”, that connects “high-growth companies with trusted and flexible executive talent”. We also suggest check out Braintrust (portfolio company), the first user-controlled talent network that connects organizations with highly skilled tech talent, who keep 100% of their market rate.

Some networks are more specialized. For example, there are several networks of financial professionals:

- Accordion Partners consultants “work alongside sponsor management teams – focusing exclusively within the Office of the CFO, (…) empowering the entire finance function – including FP&A, operational and technical accounting, M&A, and performance improvement”.

- Tatum Executive Services provides “CFOs, CIOs and senior finance professionals [to help] lead [companies] through any challenge”.

Other specialize in certain target markets. For example, BlueWave connects private equity clients with “third-party resources to meet [their] specific needs in due diligence and value creation”.

For greater insight into the average interim executive profile, consult InterimExecs’ survey.

Direct Consulting

There also exist several other ways to land consulting gigs, aside from joining the networks mentioned above. You can become an advisor to one of the major consultancies. Some maintain a database of outside consultants (e.g., PwC’s Talent Exchange). Adham Abdelfattah, an advisor to the Senior Partners at McKinsey, said, “Familiarity with technology topics is extremely valuable to become an advisor for the top firms. Tech is their Achilles heel, and they’re always looking for seasoned talent that understands both technology and management to act as advisors. Basic networking (and even cold emails) with these firms can suffice if the person has relevant expertise. All it takes is 1-2 partners to want to onboard a person as an advisor once”.

You can also affiliate with a specialty consultancy in your niche. There’s a huge world of smaller consultancies which work with outside, part-time consultants on an as-needed basis. It’s much easier to get on their “call list” than to get a full-time job. TheConsultingBench offers a database of over 600 consulting firms.

Board of Directors

When hiring their directors, boards tend to look for:

- Proven leadership experience;

- Specific skills or experience – for example, a financial background, international experience, position as active or retired CEO, experience in dealing with challenges faced by a company or CEO; and

- Network – for example, connection to potential clients.

To become a board member, you must have a history of leadership and / or management experience at the C-level. To join a board, at a minimum we recommend send your resume to all the major recruiting firms, as most top recruiting firms offer a board placement service. Building relationships with major investors in your sector will also increase your odds of getting invited to board roles.

We suggest look at these resources:

- DirectorsandBoards “provides public and private company directors, leaders and owners of multigenerational family businesses and C-suite executives with the knowledge and skills to be successful in their roles”.

- NACD (National Association of Corporate Directors)’s Accelerate program provides participants with “the tools, resources, and exposure that are essential to launching a successful career as a director”.

- FasterLandings offers a “Landing Board Seats” program to help candidates get on Boards.

- The Private Directors Association frequently hosts webinars on board-related topics (for example, “Board Responsibilities During a Pandemic” or “How to Market Yourself for a Board Seat.”)

- The Institute for Corporate Directors in Canada helps its members “perform their director role effectively and make an appropriate contribution in the boardroom (…) [by offering] professional development programs that provide value-added director education and learning opportunities.”

Currently, many boards are also aggressively seeking to become more diverse, as 61.4% of all board positions are still held by white men. The 2020 Spencer Stuart Board Index finds that currently, in S&P 500 boards, women account for 28% of directors while minorities account for 20%.

In terms of background and function, 17% of new Directors are Active (not retired) CEOs or presidents, as opposed to 26% in 2010. New Directors come increasingly more from financial backgrounds (27% in 2020 vs 21% in 2010) and functional roles (22% in 2020 vs 18% in 2010).

Useful resources for women and minorities seeking board seats include:

- Catalyst has compiled a list of “organizations and institutions that offer programs for networking, education, leadership and community” which help executive women interested in board service.

- WCD (Women Corporate DIrectors) is “the world’s largest membership organization and community of women corporate board directors”, supporting its members in “connecting with peers and advancing visionary corporate governance”.

- DirectWomen seeks to “increase the representation of women lawyers on corporate boards” by “[developing] and [positioning] women attorney leaders for board service. It also serves as a resource for companies seeking qualified women board candidates.”

- Executive Leadership Council is an organization comprising current and former Black CEOs and senior executives at Fortune 1000 and Global 500 companies. Its “Corporate Board Initiative” “builds awareness, improves readiness, and enhances the visibility of ELC members who are interested in and actively pursue corporate board service”.

Further reading

- 7 Ways to Position Yourself to Get on a Board

- Want to Join a Corporate Board? Here’s How

- Startup board meetings template presentation

- Looking for a Board Seat? Networks Are the Way to Find—and Be Found

- Ten Networking Strategies to a Seat on the Board

- Spencer Stuart’s board index (compensation data)

Senior Advisor Networks

Senior Advisors are an investor-sponsored group of senior executives who work closely with funds to source deals and / or portfolio companies to provide board service and mentor. For example, I helped build Chambers Street Executive Network, a proprietary advisor network for Goldman Sachs Special Situations Group.

This position typically requires a monthly time commitment of 2 to 10 hours. Pay will vary based on service given, and may come in as a retainer or service fee (payable directly by the company in many cases, not the fund).

Senior Advisor networks offer a low-fixed-cost, high-return talent pool option. They differ from the traditional talent sources we list above in 4 main ways:

- Duration: Typical relationship is 6 months to many years, versus 1-2 hours to 3 months for experts or permanent for recruited executives.

- Illustrative cost: Senior advisors are paid typically on a retainer, as opposed to a $1,000/hr rate for expert networks, $300-$700/hr rate for consultants, or ⅓ of compensation for hired executives.

- Driver of executive compensation: Because of the long term relationship, you can pay the senior advisor based on value created and continued involvement with client companies, instead of length of consultation (experts and consultants).

- Confidentiality: You can ask outside consultants to sign NDAs, but practically speaking they are a greater risk of information leakage than a long-term senior advisor.

Certain VC funds offer “Fellowships” for industry executives. For example, Shift’s Defense Ventures Program offers “8 cohorts of up to 25 Fellows from across the US Armed Services, (…) immersion programs focused on venture capital, the technology startup ecosystem, cybersecurity, and artificial intelligence. Next year will also see the introduction of an executive seminar, a high-impact week-long version of the Fellowship, for senior leaders of the Department of Defense and U.S. Armed Services.”

Private Equity Deal Executives

Another option is to look for a company to buy, and partner with an investor to finance that. A Deal Executive (sometimes called an Executive in Residence or Acquisition Entrepreneur) looks for a company to invest in or build, and typically serve in as CEO. The role usually pays a modest retainer with the incentive of a finder’s fee and/or CEO role in the new company. To become a Deal Executive, you typically have a history of successfully leading a company at the C-level, or as a direct report to C-level. You must also offer a deal thesis or letter of intent to a private equity/VC firm.

Private equity funds are primarily looking for deals, not executives. In order of desirability:

As a Deal Executive, you should approach PE funds with a well articulated deal thesis and position yourself as the “gateway” to this deal. It also has to be correctly scoped for it to be credible that you’ll be able to find the right deal. A good investment thesis includes a few key elements:

- Clear definition of industry, in terms of niche, size, geography, etc.;

- Transaction rationale consistent with the company’s growth prospects;

- Basic financial markets analysis – trading range, feasibility, etc.;

- Outline of value-creation opportunities and plan for pursuing them;

- Explanation as to why you and your team are ideally suited to lead the effort;

- Roster of 5-20 target companies;

- Status of discussions with targets (if any); and

- Thoughts on likely exit (IPO, strategic buyer).

Similarly, you should also present a Deal Memo, which should include:

- One-page teaser (the cover email);

- Business plan;

- Executive profile;

- Forecasts – strategic, operational and financial ones.

Private equity investors are seeking the “Three Cs” in Deal Executives: Credibility, Compatibility, and Deal-Catching:

- Credibility. To appear credible, and able to do the job, you should have previously held CEO-level positions, or have directly reported to C-level executives. Ideally, you have 10+ years in your target industry or related market and 10+ years leading P&L, preferably also balance sheet experience. For additional credibility, it’s best that you have personal capital to invest to show that you have skin in the game. The specific amount of which should be proportional to your age: a 35 year old is not expected to have is not expected to have the same amount of savings as a 50-year-old. Ideally, you would have a management team ready, corporate governance skills (board experience), as well as investor relations experience.

- Compatibility. To ensure mutual compatibility, your goals and incentives should be aligned with that of the private equity or VC fund, as well as the timeline for realizing them and exit strategy. Naturally, having some personal chemistry makes not only for a more pleasant working environment, but allows for greater synergies to be realized when working together.

- Deal-Catcher. Deal-catchers are usually entrepreneurial and sales-oriented, with a willingness to relocate, if needed. As a deal-catcher, you’re expected to proactively seek to identify deals. You should also be financially stable, and ideally have a supportive spouse, in order to be able to go without salary during the search for deals. Ideally, you would also have acquisition experience, to facilitate the process.

Partnering with operating executives is a successful strategy which is a focus for only a small number of firms, many of whom market themselves as search fund sponsors. U.S. funds whose core strategy is to partner with executives to execute a transaction and bring in new management upon investing include, for example, Broadtree Partners, Buy+Build Fund, Endurance Search Partners, Frontenac, GTCR, Housatonic Partners, NextGen Growth Partners, Pacific Lake Partners, Post Capital Partners, Search Fund Accelerator, and TDV.

Private equity/executive intermediaries are hybrids of an investment bank and recruiter, which work with executives throughout the process to help execute a transaction. Examples include:

- Blackmore Partners helps funds find executives with “Full P&L Responsibility of $100 million or more in work history. Currently employed in senior leadership positions. 10+ years of industry experience”.

- Harvey & Company is a buy side acquisition advisory and principal investment firm, that employs an “executive-first model, partnering with proven operators that bring exceptional industry experience and connections that can be leveraged to build businesses”.

- Orbit Partners “helps the best investors partner with the best advisors to successfully craft deals.”

Private equity fund / executive intermediaries have a standard process for executing transactions:

- Review the industry for feasibility by looking at market trends to identify any opportunities, conducting valuation analysis, reviewing capital-intensity requirements, conducting fragmentation analysis for opportunities to acquire smaller players in a given sector.

- Profile executives to assess candidacies, based on the three desired characteristics mentioned above.

- Source companies for the transaction.

- Source sponsors for the transaction.

The order of points 3 and 4 above is interchangeable, as an executive has two main paths to choose from in pursuing a transaction:

- Finding the company and getting close to signing a Letter of Intent, then pursuing a sponsor; or

- Finding a sponsor and then searching for a company, where the executive screens for funds with a track record of pursuing executive-led transactions and interest in industry. This strategy is even more prevalent in larger deals.

Many companies prefer to sell to management, even at risk of a lower price than they might get from an auction. Primary reasons as to why that’s the case include secrecy, continuity, speed, lower investment banking fees, and “dummy insurance” (not looking dumb for selling a company at too low a price). The selling company may prefer to keep a stake in the spunoff company, which can be easier when selling to a known party.

The process for completing a transaction has 5 main steps:

Step 1: Launch Relationship (2 – 4 weeks duration)

Reach out to funds that are in your industry and value your expertise. Hold initial meetings to begin the relationship and assess the investment thesis.

Step 2: Finalize partnership between executive and fund (1 – 4 weeks duration)

Refine the thesis with the other party and agree on compensation, economics and exclusivity. Background checks are conducted and a deal origination plan is formulated.

Step 3: Identify & Contact Opportunities (1 – 12 months duration)

There are two approaches to doing so. In the concept-driven approach, you’ll search for industry inflection points which may indicate an investment opportunity. In the opportunistic approach (network), you will network through every possible channel to find an opportunity.

Step 4: Evaluate Targets (up to 3 months duration)

The key questions to ask include:

- Can a deal be made?

- Can we interest investors?

- Can you “drive” the deal?

Step 5: Closing (up to 3 months duration)

The table below summarizes the typical economics for mid-market private equity acquisition, for private equity group (“PEG”), deal finders, investment bankers, and other executives:

| Fee Type | Payer | Amount | Recipient of Payment |

| Transaction Fees | Capital Providers | 0.5% – 3.4% of deal size* | PEG pays finder’s fee of 1-3% of enterprise value plus sometimes carry, to deal finder + buy-side investment bank (if any). (Company (specifically selling shareholders) pay investment banker seller’s fee.) |

| Monitoring Fees

|

Company | 0.2% – 4.4% EBITDA (median 1.2%)* ** | Company pays outside board members for ongoing services (~$5k+/meeting + equity incentives) |

| Expenses | Company | Post-deal expenses, not pre-deal | Company pays PEG for post-deal expenses. Important for buy-side operating exec/investment banker to get PEG to commit to pay broken deal costs. |

| Investment Rights | – | – | Usually unlimited co-invest rights for executives involved, with no PEG management fee. Executives will, however, pay pro rata monitoring/other fees. |

This does not reflect compensation for an executive’s role as a company employee post-deal. Note that transaction fee and carry are inversely related.

* Robert Seber, Dechert LLP, “Transaction and Monitoring Fees: Does Anything Go?”, 2003.

** The PEG’s fund documents will generally discuss whether a portion of that fee (often half) is set off against management fees that the LP’s would otherwise owe.

Other data based on Akoya Capital, Oberon Securities, and other interviewees.

VC Entrepreneurs in Residence

Certain VC funds proactively seek out qualified Entrepreneurs in Residence. Although the role is constantly evolving, VC EIRs are usually previously successful entrepreneurs who are building a startup leveraging the VC’s support. In addition, they may have responsibilities to support existing portfolio companies and/or evaluate potential deals. Many EIRs are compensated with zero income until they found a company, but there are some who are earning a retainer typically in the range of $90,000 to $150,000.

Among the venture capital funds with formal EIR programs are:

- General Catalyst has an XIR (Executive-in-Residence) program, where they “collaborate with world-class executives to create a new business or identify an existing growth-stage business to transform with them”.

- Foundation Capital selects several candidates to develop businesses for emerging technologies. Ani Chaudhuri writes about his experience as an EIR working with Blockchain technology.

- I have offered an Entrepreneur in Residence program for founders seeking to launch a company in my areas of interest.

Further Reading

- Inovia Capital writes about what they look for in an EIR.

- Jah Ying Chung, co-founder at The Good Growth Co., shares her experience as an entrepreneur-in-residence at Betatron, Hong Kong’s only venture-backed accelerator.

- Several ex-EIRs share their experience on Quora.

Venture Partner/VC Scout programs

Some VCs have formal “Scout” programs to compensate people for sourcing investments. One of the best known is Sequoia’s decade-old Scout program, which allocated $100k to each scout from its $180M scout fund.

Compensation for Scouts generally involves receiving a fixed fee and/or a percentage of returns for deals that go through, but no guaranteed compensation. For example, Jason Calacanis shares in his book Angel the compensation structure for Sequoia’s Scout program: 45% of returns are given to the Scout, 50% to Sequoia, and the remaining 5% to a bonus pool for other Scouts in the program. The application process for joining a Scout program can be very competitive, with some programs receiving thousands of applications per position.

Jai Malik, Venture Partner at Republic and ex-corporate Scout for Tata Communications, shares advice on becoming a Scout: “I think the most important thing they saw was that I was open to learning whatever it took to get the job done. I think that’s pretty standard with other positions. How well you can show that you are committed to what you want to achieve.” Among the other firms with scout programs: Accel, Ada Ventures, Atento Capital, Atomico, BackedVC, Bloom Venture Partners, Blossom, Chapter One, Contrary Capital, Gen Z Scouts, GGV Capital, Harlem Capital, Index, Indie VC, Kleiner, KPCB, Lightspeed, New Stack Ventures, Permanent Equity, Saison Capital, Sequoia, University Growth Fund, Upfront, and Village Global.

Some VC funds offer fellowships for students to work for portfolio companies and attend events hosted by the VC, e.g.:

- Bessemer’s Fellowship Program places students with “some of the fastest-growing technology companies in the world to acquire invaluable work experience and access to mentors, industry professionals and the Bessemer Fellows community”;

- Fellows of the 8VC Fellowship “complete a software engineering internship at an 8VC portfolio company while attending weekly Fellowship events to meet and learn from notable entrepreneurs, executives, and investors in our network from Silicon Valley and beyond”;

- The Soma Capital Fellowship allows students to “[work] for a seed-stage Soma Capital portfolio company as a design, engineering, or business intern, then hone [their] idea with Soma’s help in the incubation stage.”

For a full list of fellowships, see the VC Fellowship database.

Further reading on scout programs:

- What is a venture partner and how do I become one?

- How to hire a venture partner and how much to pay?

- Elad Gil, serial entrepreneur and ex-VP at Twitter, further shares advice on becoming a successful scout.

- Ben Casnocha provides a useful FAQ on Scout programs

- Adam Gering, currently Director of Research for a fintech company and previously Software Engineer at Microsoft, shares his thoughts on becoming a Scout for VCs.

Other resources:

- Here is the slide deck from the video presentation at the beginning of this essay:

- How to negotiate a partner role at a VC or private equity firm

- Reading list for analysts and associates in private equity/venture capital

- Microcredentials for the Effective Venture Capital or Private Equity Investor

- Venture capital/private equity compensation data and recruiters list

- Limited partner checklist for evaluating funds

- How to negotiate and evaluate your job offer

- How to write a resume that sells

* Disclosures: I’m an investor in Braintrust via HOF Capital, where I was formerly a Managing Partner.

I published an earlier version of this essay in Techcrunch. Thank you to my co-author for this essay, Paulina Symala, a Consultant at Oliver Wyman and a past intern.