You’ve probably read dozens of articles about how to raise capital from venture capitalists. However, as a VC, we have the opposite problem: how do we originate companies in which to invest?

It might appear that origination is becoming much easier because of new tools like AngelList and the SEC moving toward adoption of rules that will allow equity based crowdfunding. Just do a search online and the VC’s job is done! But in practice, these phenomena create a tremendous volume of startups, which investors then have to filter. The easier it is to source, the more you have to work to screen.

Most investors rely on their network of colleagues and service providers to source investments. Unfortunately, our research finds this traditional approach is not powerful enough to uncover all of the most promising investment opportunities.

Prior to joining ff Venture Capital, I published the first-ever study of how private equity and venture capital funds originate new investments, with my coauthor Chris Farmer, CEO of SignalFire and an experienced VC. We drew on our work with leading institutional investors and in-depth interviews with over 150 funds. We published the full report in the Journal of Private Equity; it’s now the #2-most viewed article in the Journal’s history. Now that I’ve been an institutional VC for a few years, I thought it would be helpful to revisit our findings from the investor side of the table.

The venture capital industry is continuing its evolution from an upside-down pyramid (typically 3-10 Partners, plus some administrative support) to a traditional hierarchical pyramid. Out of 5,923 investment professionals in our dataset, 916 (15.5%) were focused primarily on origination and marketing. This is a significant increase over the percentage a decade ago, and reflective of the broader trend towards increasing specialization by function. Similarly, my research on venture capital portfolio operations found that Portfolio Operator VCs such as Andreesen Horowitz, First Round Capital, ff Venture Capital, and Google Ventures are hiring unusually large teams and structuring them in traditional pyramids.

Deal origination is a slow, labor-intensive, frustrating process. The median VC reviews 87 opportunities before making 1 investment. I’ve shown below some specific data from a range of VCs

Annual Deal Pipeline for Selected VCs and Angel Investor Groups

|

Acquirer/ Investor |

Angel groups using Gust (2010)[i] |

ff Venture Capital |

First Round Capital (2009)[ii] |

TA Associates (2006)[iii] |

Highland |

| Investing focus |

startups |

startups |

startups |

growth companies |

growth companies |

| Profiled initially |

20,850 |

NA |

NA |

NA |

NA |

| Target Selected |

1,315 |

~2,000 |

8,000 |

8,000 |

10,000 [v] |

| Met |

1,047 |

1,000 |

750 |

750 |

1,000 |

| Negotiated with |

NA |

~25 |

NA |

NA |

NA |

| Detailed due diligence |

577 |

~18 |

NA |

NA |

NA |

| Acquired/ invested |

541 |

10 |

10 to 12 |

10 to 12 |

10-20 |

| Deals as % targeted companies |

33.5% (2.1% of submissions) |

0.5% |

0.1%-0.2% |

0.1%-0.2% |

0.1%-0.2% |

Based on our study, we have five recommendations to dramatically improve the volume and quality of dealflow for venture capital investors.

1. Build a specialized outbound origination program.

Investors with dedicated, large-scale sourcing teams are almost all top-quartile performers across stage, vintage, and sector. The largest practitioners of these programs – including Battery Ventures, Great Hill Partners, Insight Venture Partners, Platinum Equity,Summit Partners, TA Associates, and TCV — typically have between 0.75 and 1.25 dedicated deal sourcers for every generalist investment professional.

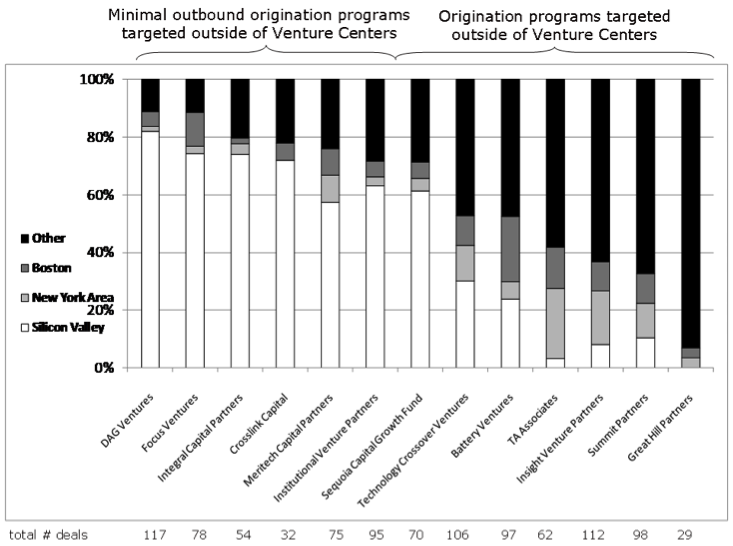

I’ve shown below a case study of the geographic diversification of the largest late-stage technology venture capital / growth equity investors. The funds with sophisticated non-venture center outbound origination programs were almost all able to raise funds equal or larger than their preceding fund in the economically challenging period 2007-2010. They are typically among the top quartile performers. These funds use a combination of cold-calling, travel, firm networks, paid expert networks, and technology to identify investment opportunities outside of their neighborhood. The funds with more traditional origination are primarily focused on their local venture center network.

Leading Late-Stage Technology Investors’ Portfolio by Geography, 2001-1Q2010

Notes: Only for IT & related sectors. Battery & Sequoia data only include late stage/growth equity deals.

Similarly, Professors Henry Chen, Paul Gompers, Anna Kovner, and Josh Lerner found in a research paper, “Buy Local? The Geography of Successful and Unsuccessful Venture Capital Expansion” that the best performing VC funds are based in the major venture centers (Silicon Valley, Boston, and the New York area), but their best investments are outside of those geographies. Their late stage deals outside of the venture centers outperform by ~5% vs. those in the venture centers; early stage deals outperformed by ~4%. To get access to these investments outside of the major VC centers, you need to proactively market in those geographies beyond bicycle range.

By analogy, look at a middle market private equity firms such as the Riverside Company. They have developed a broad network of 24 senior, focused deal originators to produce top quartile results in 8 of their 9 recent funds. Summit Partners and TA Associates have leveraged their origination programs to move into later stage buyouts. Other private equity firms have created a formal advisor network to augment their in-house origination teams, including 3i’s Business Leaders Network and Goldman Sachs Special Situations Group’s Chambers Street Executive Network.

My preferred primary origination strategy is to provide a high level of services to entrepreneurs, and then let word of mouth spread. We’d rather spend more energy working with our companies after we invest, rather than working to meet them prior to an investment. While certainly active in our New York tri-state home region, ffVC does invest without regard to geography. Out of over 70 companies that ffVC has invested in since 1999, about 20 are in New York. ffVC has three in Israel, two in Canada, one in the UK, and the remainder scattered all over the US.

2. Create opportunities, instead of waiting for opportunities to appear.

A number of the funds we studied use an origination approach that allows them to proactively co-create companies or opportunities. Benchmark Capital and General Catalyst Partners work with Entrepreneurs-In-Residence (EIRs) to develop their ideas, giving such VCs an advantaged position to lead an investment in any resulting company. Private equity funds such as Castle Harlan and Blackstone Group frequently partner with leading corporations when bidding on investments, allowing them to bring unique value and resources vs. other possible investors. Private equity fund Frontenac Company uses a “CEO1ST” strategy, partnering with “deal executives” to source investments in these executives’ focus industries.

My Partners and I do have strong opinions on the direction in which technology is evolving. However, we believe in looking at companies first and evaluating them against the thesis the founders articulate, vs. going in with a thesis and looking for companies that fit the thesis. Our job is to invest in the growth areas of 2018. The people who know the most about the growth areas of 2018 are not VCs (i.e., glorified commercial bankers) sitting behind a desk. They’re the entrepreneurs on the cutting edge of their respective disciplines. We just need to assess each entrepreneur against our decision criteria.

3. Look for targets with revealing “tells”.

One of the great challenges of investing in private companies is that most private companies do not want an outside investor. In order to filter the universe of companies, some investors specifically reach out to companies bearing “tells” that the firm would welcome an outside investor. Some VCs monitor Internet traffic reports or job boards to see which companies are growing. Firms like CBInsights, Bright*Sun, CDling, Crunchbase, DataFox, Indicate, Inkwire, Mattermark, Privco, and OnlyInsight help to automate this for VCs.

Many private equity funds we interviewed for the Journal of Private Equity study view a CEO over age 60, or a family-run company that hires an outside manager, as a tell that the firm may welcome an outside investor. As data about public companies and private companies becomes increasingly searchable, investors can more sharply target their outreach. Companies like PrivCo and Navon Partners (my old startup) are working on automating this signal identification process.

We do not use any of these automated services currently (although we’re evaluating some). We have such a deluge of inbound deal flow via our network that we are not investing a lot of energy seeking out additional companies to filter. However, of the companies that approach us, we are very sensitive to the “tells” that indicate a given company has high prospects of success.

4. Become open and transparent.

Historically, institutional investors kept their investing strategy very discreet. However, that model has now flipped. About 10-15% of the 1,000 active venture capitalists blog, according to Jeff Bussgang, General Partner, Flybridge Capital Partners. Some firms, such as Formation 8 and Khosla Ventures, post analyses of their target investment sectors on their websites. These investors have found that openly discussing their investment theses increases their perceived expertise and trustworthiness, and thus generates dealflow. ffVC has an active blog and I keep a personal one at teten.com.

While relatively few private equity firms are so open today, Norwest Equity Partners regularly publishes thought pieces. HealthPoint Capital has made their website a destination for M&A/investing information in their target industries, the musculoskeletal sector — specifically orthopedics and dental. MCM Capital (case study) is a rare example of a lower middle-market private equity fund with a proactive social media strategy.

5. Take advantage of social media and emerging platforms such as AngelList.

Many investors report that they used LinkedIn, Twitter, Facebook, and like tools to keep in touch with their professional and personal networks. However, those tools do not address all the unique needs of a VC. Specialty tools like Angel List, Gust, SeedInvest, and OurCrowd are emerging as potentially significant tools for sourcing early-stage investments.

That said, our experience so far is that these online markets are most useful to identify opportunities to join a syndicate, not to source and lead a new investment. To date, ffVC has sourced only one investment on Angel List, in 500px, where ff led the seed round after being seduced by 500px’s beautiful site.

All of these services want to create a liquid market for early-stage private companies, because that would be a very powerful position to be in. The challenge is that the most desirable members of a market often want to go off-market, for the sake of speed, discretion, and (important) a perceived sense that they do not need to go to the market. Some early-stage startups are a luxury good; some investors will pay a premium for perceived exclusivity.

The best entrepreneurs historically tend to go direct to their historical and/or most desired investors, with whom they already have a relationship or with whom they can readily obtain a relationship. Once that lead investor is in place, then these online tools are very valuable for filling out the round.

The online markets are therefore likely to attract many companies that are not very attractive to investors (at the time of finding a lead), both because of their openness to all comers, and because of the selection bias.

Historically, ffVC has had much better returns by investing in “cold” deals than hot deals. ff believes there is no correlation between “heat” of a company at the time VCs come in, and its eventual success. Think Color or Airtime, which were well funded and high profile and within months lost their momentum. Despite the fact that the out-of-favor deals can be some of the biggest winners, my instinct is that the majority of companies in a completely open market are unattractive and bad investments, as opposed to unattractive and contrarian good investments. Therefore, using these systems necessitates a lot of time filtering.

Similarly, Harvard Business School Alumni Angels of Greater New York currently uses Gust to run our backend. Although HBS Alumni Angels welcomes cold applications via our website, every company in which our members have invested to date came via referral. In 2013 HBSAANY launched a Fast Track program, which allows our members who are investing in a company to rapidly find other members who want to join the syndicate. This has to date a nearly-100% success rate of sourcing new investors, vs. our lower success rate in providing funding to companies that come to our conventional pitch nights.

By analogy, when you’re looking for a date, most people first will think about people in their school/workplace whom they already know. Only if no one appropriate comes to mind will people consider using other tools to find a partner. And if you’re highly desirable on the marriage market (think, supermodel), you probably have a lot of offers even without going onto an online network.

We are in the early days of the development of online markets such as AngelList, and these online markets are led by savvy people who are well aware of the delicate dynamics of creating a real marketplace. I’m looking forward to seeing how they evolve.

For investors in later-stage private companies, players such as the Association for Corporate Growth’s online network; Axial; Dealmarket, IntraLinks (which acquired MergerID and PE-Nexus); MergerMarket; and SecondMarket are all attempting to bring technology and efficiency to the origination process. The private equity universe is much slower to adopt technology than the VC world.

However, as the millennials reach decision-making roles in companies, an increasing number of senior executives and investors are actively participating in gated online communities. An example is the International Executives Resource Group, an online community only open to executives who were C-level (CEO, COO, etc.) or reported to a C-level executive, and earned a minimum of $200,000. In the long run, I foresee that the private equity world will be impacted by online platforms in the same way that AngelList, Gust, and their peers have impacted the early-stage world.

___________________

Notes

For their help in our research, I particularly want to thank Chris Farmer; my former colleagues at Evalueserve as well as our research associates Yujin Chung (now a Partner, Andreessen Horowitz) and Neha Kumar. In addition, thank you to our interns Dan Clark, Nitin Gupta, and Nikhil Iyer.

[i] From http://angelsoft.net/a/venture-valuation, as of twelve months ending March 17, 2010.

[ii] Aktihanoglu , Murat. “NYC Entrepreneur Week Events Take-aways.” May 3, 2009.http://centrl.com/blog/?p=53.

[iii] Rudd, Amber. “A Kind of Magic.” Corporate Financier, October 2006.

[iv] Economist, Global Heroes: A Report on Entrepreneurship, March 14, 2009., p. 9. “Targets selected” figure indicates number of business plans received.

[v] Number of business plans received.

Also published in Forbes. Photo credit: 500px/Andreghan.