(co-written with Stephane Nasser, co-founder of OpenVC, an open-source initiative to collect and analyze all VC theses.)

VCs love to talk investment theses: on Twitter, Medium, Clubhouse, at conferences. And yet, when you take a closer look, theses are often meaningless and/or misleading.

OpenVC is a new, open-source initiative to collect and analyze all publicly available VC theses, to help founders more efficiently find the right investors, and vice-versa. For the first time, we are sharing here our initial learnings. We hope you’ll upload your own thesis to benchmark yourself. We’ve identified 6 common patterns of how VCs articulate their theses, and some best practices in doing so.

Our analysis is based on two complementary datasets:

- 125 theses so far submitted by investors into the OpenVC database

- 36 theses pulled directly from US VC websites by David Teten and Sam Sabin, co-founder, Hireblue.

Our four primary learnings:

- Public theses are often inconsistent with how firms actually deploy capital.

- VC theses are often so vague that they’re meaningless.

- We found six categories of VC theses, plus a 7th: the non-thesis.

- Investment theses are just hypotheses; the portfolio shows how accurate the hypothesis was.

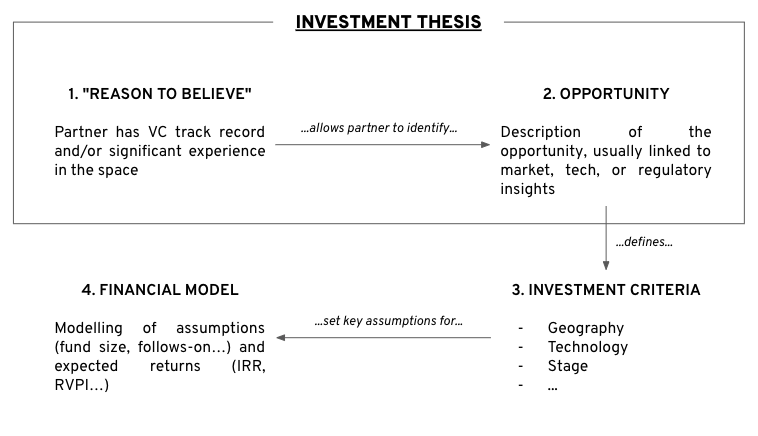

For the sake of simplicity, we will consider “investment thesis” and “investment criteria” as equivalent terms moving forward, although we argue that the thesis leads to the investment criteria. We summarize how they interrelate in the table below.

1. Public theses are often inconsistent with how firms actually deploy capital.

A typical VC thesis: “we invest in tech startups in Europe at an early stage”. However, our experience shows that in many cases:

- “Europe” means a handful of countries, for instance, France, UK, and Germany

- “Tech” means B2B Saas/Fintech or Consumer apps

Thirty-four VC firms in OpenVC call themselves “early-stage”. Yet, 30% of those don’t actually invest in pre-revenue startups. The phrase is quite ambiguous. We suggest quantifying check size so that your investment preference is clearer.

Almost every VC says that they invest in the “best” founders. However, according to PitchBook Data, since the beginning of 2016, companies with women founders have received only 4.4% of venture capital deals. Those companies have garnered only about 2% of all capital invested. This is despite the fact that the data says that in fact you’re better off investing in women.

This lack of transparency results in confused founders who chase the wrong investors. In turn, investors are overwhelmed with poorly qualified opportunities.

2. VC theses are often so vague that they’re meaningless.

Chris Janz from Point Nine Capital wrote on Twitter:

The modal VC thesis is: “We invest in great teams addressing large markets with disruptive solutions”. Who invests in lousy teams addressing tiny markets with outdated solutions? Theses also tend to use the same words across many firms, e.g., “daring” and “bold”.

In particular, in our second dataset, we found a disproportionate number of theses focused on “technical” companies (vaguely defined) and focused on companies attacking “problems of the future rather than the present”, in various permutations of that language.

| Top Visible Heuristics (in dataset of 36 US VCs) | Occurrences |

| “Technical” Companies (i.e. any mention of a focus on tech companies) |

26 |

| Local affinity or bias |

10 |

| Attack problems of the future rather than the present (or some variant) |

9 |

| Technical founders |

7 |

Why are the investment criteria so imprecise on the VC websites? We have three theories, in descending order of importance:

- Option value. Investors don’t want to be too restrictive and miss out on a deal. However, we’d argue that for most smaller managers who are not brand names, it’s better to be highly identified in your niche than being a generalist. Most LPs we speak with agree.

- A desire to look ‘sexy’ and politically correct as opposed to being honest. This is probably a major reason. For example, saying publicly, “We invest mostly in White/Asian men people who went to Stanford like us”, accurately describes numerous VCs, but doesn’t sound very politically correct.

- VCs are afraid to give out their secret sauce. We think this doesn’t make much sense; you can share your criteria without telling the whole logic behind. Many top-tier VCs share detailed public theses.

3. We found seven categories of VC theses, plus an 8th: the non-thesis.

What makes an excellent – or at least clear – investment thesis?

Typically, investors either have a very loose non-restrictive strategy to investing, or maintain a strict focus on a few particular areas. As two extremes:

- Founder Collective says, “Founder Collective is deliberately anti-thematic. Visionary founders have shown us that the weird use cases of today can become the hot themes of tomorrow.”

- By contrast, Right Side Capital has a very tight thesis:

- “Check Size: $50K to $200K. Vast majority $100K to $150K.

- Total Round Size: $50K – $500K. (Occasional exceptions to $1M.)

- Valuation: $1M – $3M. (Rare exceptions to $6M with extreme traction.)

- Traction / Progress: Almost always $5K to $30K/month in gross profit. No ideas or prototypes.

- Sector: Anything in tech. But you must be doing real engineering of some kind.

- Headcount: Usually at least 2 full time founders. Often a few full or part time workers.”

We take from this that there is little consensus on whether VC investing should be thesis-driven or not. And even the “thesis-driven” VC firms often make investments outside of their stated thesis.

Of the firms that articulate a thesis, most fall into one of, or a combination of, the following six buckets:

1) Industry funds. Warren Buffett famously stated that “diversification is protection against ignorance. It makes little sense if you know what you are doing.” In venture capital, the industry- or sector-focused funds specifically disavow diversification:

- Andreessen Horowitz, which is a generalist as a whole, has launched dedicated funds across Crypto, Bio, and Fintech.

- AgFunder, focused on the Food and Agri sectors, to solve for challenges brought by climate change, failing soils and population growth.

- Foundry Group, investing primarily in “Software and Internet”, follows six major themes, e.g., Human Computer Interaction (HCI) or Distribution.

- USV invests in companies that increase “access to knowledge, capital, and well-being by leveraging networks, platforms, and protocols”.

Data from OpenVC shows that VCs typically focus on 2 technology classes. Software is by far the most sought-after class, with 94% of VCs investing in it. Deep tech follows as a distant second with 57%. Hardware and therapeutics are lagging well behind.

Out of 125 funds in the database, 33 state they invest in 1 type of technology (e.g. “software”); 43 invest in 2 types of technology (e.g., “software” and “deeptech”), and so on.

2) Business model-defined funds. For example, Point Nine Capital focuses on B2B SaaS and marketplaces at the seed stage, across many industries. These firms also sometimes target startups that serve a specific kind of customer (e.g. B2B vs B2C) within the business model preference.

3) Geography-defined funds. These tend to fall into two main categories:

- VCs investing in specific geographies. Avataar Ventures invests exclusively in companies which fit these criteria: “$15 Million + in Annual Recurring Revenues; Strong Tech-Led B2B & SaaS Companies; Core Operations in India/ South East Asia; Open to Active Partnering.” In 2019, according to the CVCA, Real Ventures invested in 42 rounds, with the total value of those rounds equal to that of the next three most active private VC firms combined. Real sees 80% of all seed deals in Canada.

- VCs investing abroad or in binational companies, typically with technology based in a 2nd or 3rd tier market, and sales/marketing in a 1st tier market. Data from OpenVC suggests that 75% of funds invest in more than 1 country. These results are consistent for both US-based and Europe-based VC firms. See Why venture capitalists are investing in international startups and Why international startups love NY, and why NY VCs love international startups.

4) Entrepreneur-defined funds. These firms focus on certain management philosophies or categories of founders.

- Female Founders Fund, AmplifyHer Ventures, Halogen Ventures, and many others invest exclusively in women-founded businesses.

- a16z’s Cultural Leadership Fund aims to “enable more young African-Americans to enter the technology industry.”

- J-Angels “is a community and a VC fund of top American investors (Jewish-American & Israeli-born) in Silicon Valley and San Francisco.”

- Diaspora Ventures is a “pre-seed fund … looking to back the next generation of French entrepreneurs building tech companies in the US.”

A special subset of this are investors which focus on mission-driven founders, and typically have explicit ESG criteria. For example, City Light VC says, “We only invest in companies where there is a direct relationship between financial outcomes and measurable social impact.”

5) Structure-defined funds. Revenue-Based Finance and Flexible VC investors invest using “alternative VC” structures, as opposed to conventional preferred equity and convertible notes. Most of these firms state categorically that they exclusively invest using these models, in order to reduce the process friction of explaining their model to companies which may not be comfortable with it.

6) Situation-defined funds. Some firms optimized around certain aspects of the investment situation. Alpha Partners and Proof provide capital when their partner VCs don’t have pro rata, and share the economics on the investments. Correlation Ventures invests in under two weeks when there is “at least one other venture capital firm also making their first investment into the company.” John Gannon, Founder of VC Careers and GoingVC, lists these situational strategies:

- “Everybody’s friend” – Invest in the best companies you can find, no matter how small the allocation you’re given. And hopefully 🤞🏻 earn the privilege to invest more in later rounds.

- “Follow the GPs” – LPs doing direct co-investments in rounds alongside the GPs they’ve backed.

- “Index the Best” – Only invest in companies that have brand name firms on the cap table and/or as leads.

- “Round Pricers” – Have heard of at least one firm who makes their bones by pricing rounds…even though their check size is a lot smaller than you’d expect from a ‘lead’. (HT to Sunil Dhaliwal for having shared with me that this is a thing)”

7) Stage-defined funds. These funds tend to focus their investments in startups at a specific stage or seeking a certain check size. First Round Capital invests in rounds up to Series A and is often the “first money in”, backing entrepreneurs at the first stages of the company they’re creating.

4. Investment theses are just hypotheses; the portfolio shows how accurate the hypothesis was.

We cannot formally prove a priori whether one thesis is better than another. They exist as heuristics, but at the end of the day, deal flow trumps everything. If a fantastic opportunity shows up, most VCs would invest, regardless of their thesis.

Investment thesis are marketing assets towards LPs and startups. As such, there are 3 stakeholders when building a thesis: the investing Partners, the LPs and the founders.

We can see in the example above how the thesis is not “pure” from the GP point of view. It incorporates influences from the LP and, more and more, from the founders.

Faced with the daily deal flow, the investment thesis feels like nothing but “a set of strict rules, loosely applied”. Does it mean the investment thesis is just an irrelevant practice that should be ignored or abused? We think not.

In the battle for deal flow, the thesis is at the core of a fund’s value proposition. It’s part of a VC brand and identity. It’s what makes it unique and distinctive.

We’d argue that for most smaller firms, it’s better to be highly identified in your niche than being a generalist. A fund should aim to be identified as “the” specialist in one or a combination of the six buckets listed above. Alexander Jarvis, startup mentor, said, “Even at a later stage, it’s better to be talked about something than nothing at all. You can always mention you do other things later, as they reach out knowing you are awesome at something.”

Most important, ideally show your data: number of checks written at each stage; number of checks in each size level ($500k-$1m, $1m-$5m, etc.); follow-on ratio; etc. Almost every investor is glad to share the (winners in their) portfolio, but only a few will share detailed analytics. Some worthwhile examples are First Round Capital’s 10 Year Project and FJ Labs 2020 Year in Review.

Alexander Jarvis observes, “VCs bury their dead quietly; they write medium posts when things went well.” We hope more firms over time will feel comfortable sharing the real data as to how their data lines up relative to their investment thesis…and their investment hypotheses.

Further reading

To see some other examples of comprehensive public theses, we suggest looking at (among many others):HOF Capital (where David Teten was formerly a Managing Partner); Sequoia Capital (focused on people not business); and Scale Venture Partners.

Disclosures: David Teten has advised Real Ventures and Right Side Capital. Thanks to Paulina Symala and Prabhat Gusain for research and analytical help, and to Alexander Jarvis for detailed and thoughtful comments. Previously published in Techcrunch.